Market Analysis

U.S. Inflation Reaccelerates as Warsh Enters the Fed

May 13, 2026

share_this_article

back_to_articles

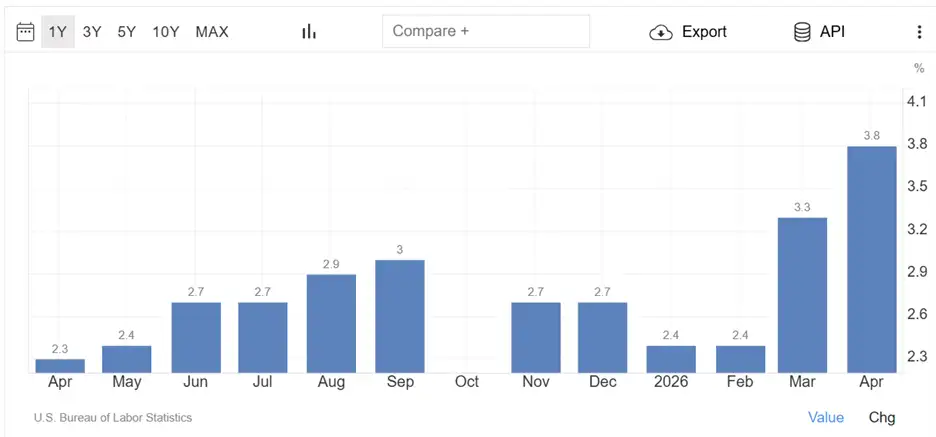

U.S. inflation jumped again in April, with CPI rising 0.6% month-over-month and 3.8% year-over-year, the highest annual rate since May 2023. Core CPI also rose 0.4% monthly and 2.8% annually, showing that inflation pressure is spreading beyond energy.

Key Drivers

- Energy prices rose 3.8% in April

- Gasoline prices surged 28.4% year-over-year

- Food prices increased 0.5%

- Shelter costs rebounded 0.6%

- Airline fares rose 2.8%

- Apparel and household furnishings also moved higher

The Iran-related energy shock remains the main headline driver, but the rise in shelter, services, and tariff-sensitive goods suggests inflation is becoming broader and more persistent.

Pressure on Consumers

Real average hourly wages fell 0.5% in April and declined 0.3% from last year. This means inflation is once again eating into wage gains, reducing purchasing power and increasing pressure on middle- and lower-income households.

Fed & Warsh Implications

Kevin Warsh returns to the Federal Reserve with a “regime change” agenda, aiming to reform how the Fed makes decisions, communicates policy, and uses its balance sheet.

His main priorities include:

- Reducing reliance on forward guidance

- Encouraging more internal debate at Fed meetings

- Shrinking the Fed’s balance sheet

- Using interest rates as the main policy tool

- Refocusing the Fed away from what he sees as political overreach

Warsh has recently aligned more with calls for lower rates, but the inflation rebound makes that position harder to defend.

With CPI accelerating and energy prices feeding into broader inflation, the Fed may be forced to stay restrictive for longer.

Asset Market Impact

- Equities: Higher inflation and rising yields are negative for growth stocks, especially rate-sensitive tech names, but as earnings are doing well this risk can fade short term.

- Bonds: Treasury yields may remain elevated as markets price in fewer cuts and a higher inflation premium.

- USD: A more hawkish Fed path could support the dollar, especially against currencies where central banks are closer to easing.

- Commodities: Oil remains the key inflation risk, while gold could stay supported by geopolitical tension and policy uncertainty.

- Credit: Higher rates and weaker real wages could pressure lower-quality credit if consumer stress increases.

Market Takeaway

April’s CPI report makes the Fed’s path more complicated. Inflation is moving away from the 2% target, consumers are losing purchasing power, and Warsh is entering the Fed with a reform agenda at a moment of intense political pressure.

For markets, this means a longer period of higher rates, elevated bond yields, stronger inflation sensitivity, and more volatility across risk assets.