Market Analysis

Trade Tensions Meet Earnings Season: Trump’s Tariffs Collide with Wall Street’s Q3 Outlook

Oct 13, 2025

share_this_article

back_to_articles

Global markets are starting the week unsettled after U.S. President Donald Trump revived the trade war narrative, threatening to impose 100% tariffs on Chinese goods starting November 1. The move came in response to Beijing’s expansion of rare earth export restrictions, a critical sector for global manufacturing and technology supply chains. While Trump attempted to reassure investors on Sunday, saying “Don’t worry about China, it will all be fine,” the escalation is already rippling through risk sentiment.

- Tariff Threat: 100% tariffs to take effect Nov. 1, on top of existing duties.

- Beijing’s Move: Expanded rare earth export controls, tightening foreign cooperation rules.

- Trump’s Tone: Downplayed escalation on social media, framing Xi’s policy as temporary.

- China’s Response: Ministry of Commerce stated it “does not want but is not afraid” of a trade war.

- Market Reaction: Broad equity selloff Friday as investors reassessed inflation and policy risks.

This development lands at a critical moment for markets. An ongoing government shutdown has already disrupted key data releases, while several Fed officials, including Chair Jerome Powell are scheduled to speak this week, making trade rhetoric a significant driver of volatility.

- Shutdown Impact: Retail sales, inflation, and housing data releases delayed.

- Fed Calendar: Powell and other governors to speak; Beige Book release Wednesday.

- Liquidity Note: Bond markets closed today for Columbus Day; equity markets remain open.

Wall Street’s Big Banks Prepare to Kick Off Q3 Earnings

At the same time, U.S. banking giants are set to open the third-quarter earnings season, providing crucial insight into the health of corporate activity, trading revenues, and credit conditions. Street expectations point to a solid quarter, with profit growth estimated around +6% year-on-year among the six largest banks.

- Tuesday (Oct 14): JPMorgan, Citigroup, Goldman Sachs, Wells Fargo

- Wednesday: Bank of America, Morgan Stanley, ASML

- Thursday–Friday: Schwab, BNY Mellon, U.S. Bancorp, American Express, State Street

For most banks, trading and investment banking divisions are expected to post their seventh straight quarter of growth, supported by active capital markets, higher policy rates, and a rebound in corporate dealmaking. Equity performance reflects this resilience: JPM, GS, C, and MS are up between 23% and 40% YTD, comfortably outperforming the S&P 500.

- Drivers of Growth:

- Robust trading & IB activity amid geopolitical shifts

- Improved lending margins from higher rates

- Easing capital rules supporting profitability

- Key Watchpoints for Investors:

- Forward guidance on tariffs and macro risks

- Commentary on deal pipelines and lending growth

- Expense outlook, particularly compensation costs

- Credit quality trends if uncertainty persists

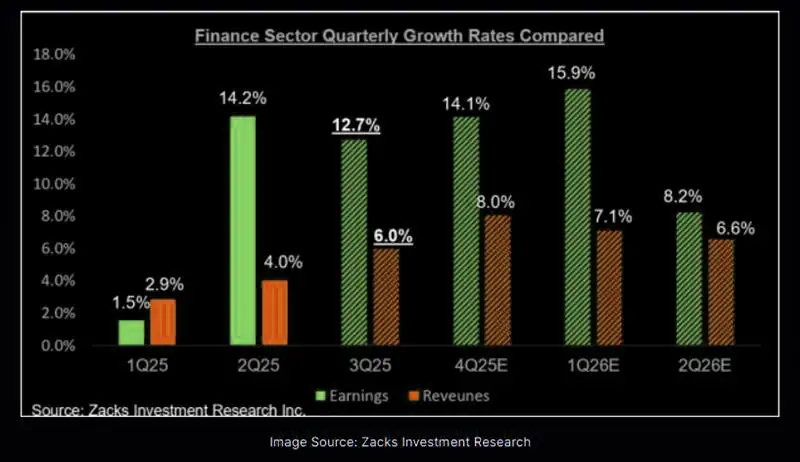

The sector’s results will shape sentiment heading into the latter part of October, especially as markets juggle tariff headlines and policy signals.Finance Sector Growth Outlook: Chart Analysis

The chart below, sourced from Zacks Investment Research, illustrates the finance sector’s quarterly earnings and revenue growth rates from 1Q25 through 2Q26E. It highlights a clear acceleration in earnings momentum, which has consistently outpaced revenue growth is a sign of margin expansion and operational leverage.

- Q2 2025 Surge: Earnings growth jumped to +14.2% vs. just 1.5% in Q1, while revenues climbed 4%.

- Mid-2025 Resilience: Q3 and Q4 earnings expected at 12.7% and 14.1%, far above revenue growth (6.0%–8.0%).

- Peak Ahead: Earnings projected to hit +15.9% in Q1 2026, then moderate to 8.2% in Q2.

- Revenue Normalization: Revenue growth stabilizes between 6%–8% in 2026, suggesting a shift from explosive top-line expansion to steadier profitability.

This trajectory underscores why investors are watching bank earnings so closely this week: strong fundamentals are colliding with rising macro risks. Tariff shocks could undermine the optimistic earnings path if they spill over into credit, investment banking pipelines, or cost inflation.

Strategic Takeaways

The convergence of renewed tariff tensions and a pivotal earnings week creates a binary setup for markets:

- A strong set of bank earnings and confident guidance could anchor sentiment and sustain equity momentum.

- Escalating U.S.–China trade tensions could reignite risk-off flows, pressure margins through higher input costs, and complicate the Fed’s policy path.

- The finance sector remains in a solid earnings growth cycle, but headline risk now poses a clear near-term threat to valuations and volatility.

In short: Fundamentals are strong, but geopolitics may override them in the short run. Markets will be highly sensitive to both Trump’s trade rhetoric and bank executives’ tone on guidance over the coming days.