Market Analysis

Markets Focus on Inflation Outlook and Central Bank Signals

Jun 24, 2026

share_this_article

back_to_articles

Investors await a crucial U.S. inflation report while central banks navigate persistent price pressures and shifting geopolitical risks.

PCE Inflation Report in Focus

The primary event this week will be the release of the U.S. Personal Consumption Expenditures (PCE) Price Index, the Federal Reserve’s preferred measure of inflation. Consensus expectations point to headline PCE rising to 4.1% year-over year, while core PCE is expected to remain elevated near 3.3%.

Key Expectations:

- Headline PCE: 4.1% y/y

- Core PCE: 3.3% y/y

- Monthly PCE: +0.5%

- Monthly Core PCE: +0.4%

Recent increases in energy prices and resilient services inflation have kept overall price pressures above the Fed's target. While economists generally expect inflation to peak around current levels before moderating later this year, the upcoming report will provide a critical assessment of whether disinflation is resuming or stalling.

What It Means for the Federal Reserve

A stronger-than-expected inflation reading would reinforce concerns that inflation remains too persistent, potentially supporting the case for additional policy tightening later this year.

Markets have already shifted toward a more hawkish outlook following recent comments from Fed Chair Kevin Warsh, with investors increasingly pricing the possibility of further rate hikes. A firm PCE report would likely push Treasury yields and the U.S. dollar higher while weighing on risk assets.

Conversely, signs that inflation is beginning to cool could ease pressure on policymakers and reduce expectations for additional tightening.

Market Implications

- Higher PCE → Higher rate hike expectations, stronger USD, higher yields.

- Softer PCE → Reduced tightening expectations, support for equities and risk assets.

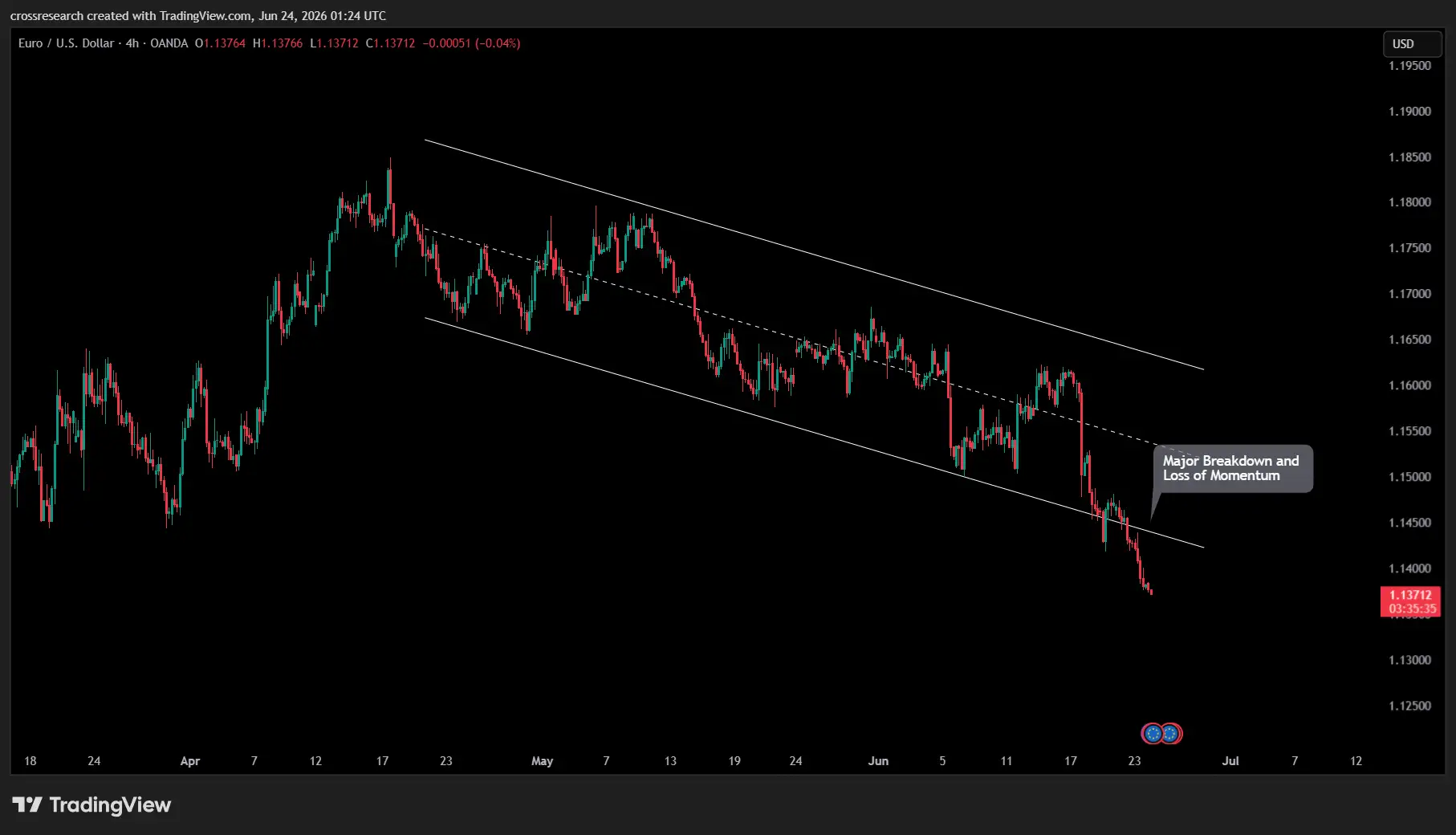

ECB Signals a More Cautious Approach

In Europe, ECB President Christine Lagarde adopted a relatively dovish tone, suggesting that additional monetary tightening may not be necessary despite recent geopolitical tensions and energy market volatility.

Lagarde emphasized that inflation is expected to return toward target over the medium term, indicating confidence that current policy settings remain sufficiently restrictive. Her comments weighed on the euro and contrasted with the increasingly hawkish expectations surrounding the Federal Reserve.

The divergence between the ECB and the Fed remains a key theme for currency markets, with policy expectations continuing to favor the U.S. dollar.

Market Outlook

Financial markets remain focused on three major themes:

- The trajectory of U.S. inflation through the PCE report.

- The Federal Reserve's response to persistent price pressures.

- Diverging policy paths between the Fed and the ECB.

The inflation data released this week will likely determine whether markets continue to price a more aggressive Federal Reserve or begin to anticipate a return toward a disinflationary environment in the months ahead.

related_articles

Market Analysis

Wall Street Earnings Preview: Banks Take Center Stage as Investors Search for Clues on Growth, Rates, and Market Direction

Jul 13, 2026

Market Analysis

FOMC Preview: Warsh’s First Fed Meeting Could Redefine Monetary Policy

Jun 17, 2026

Market Analysis

Week Ahead: Inflation, Central Banks and the Dollar in Focus

Jun 8, 2026